EU and US Face Structural Barriers to Potato Growth, RaboResearch Finds

The European Union and the United States face structural challenges in expanding potato yields and cultivated area, even as global demand for processed products accelerates, according to new analysis from RaboResearch.

The World Potato Map, published by the research division of Rabobank, shows that between 2019 and 2024 the export value of frozen potato products rose sharply from $7.7 billion to $13.2 billion. This growth was driven by higher consumer demand for processed potatoes, alongside increased production costs worldwide.

“Both a growing market and higher prices drove the surge in export value, as costs for growing and processing potatoes increased substantially across the world,” said Cindy van Rijswick, global strategist for fresh produce at RaboResearch.

The study highlights that markets such as China and India, once net importers of frozen potato products, have rapidly expanded their processing industries and are now emerging exporters. China’s potato processing industry registered a compound annual growth rate of 79% between 2019 and 2024, while India and Egypt followed with 45% and 16% respectively.

These shifts underline a broader transformation in global consumption, with frozen fries and other processed products gaining traction in regions far beyond traditional markets in North America and northwestern Europe. Imports increased in countries such as the US, the UK, Mexico, Saudi Arabia, Germany, and Spain.

Despite this global expansion, Europe and the US face limits on further yield improvements. “Rising costs have affected every player in the global potato supply chain, from growers to processors to consumers,” van Rijswick noted. Costs for seed, raw potatoes, energy, and inputs have placed pressure on profitability, even as output rises.

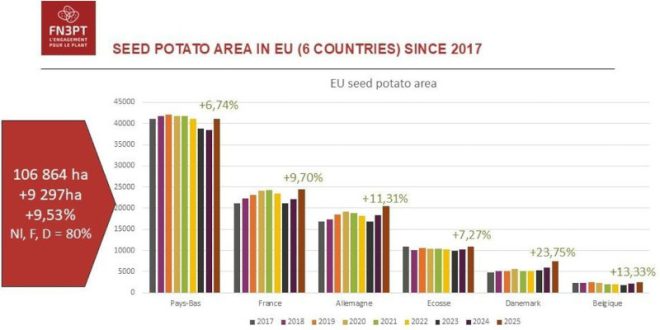

The Netherlands remains the dominant exporter of seed potatoes, accounting for about half of global shipments. But RaboResearch warns that regulatory constraints on crop protection, water quality, and the effects of climate change will make it increasingly difficult to maintain this leadership.

Global potato production reached an estimated 372 million metric tonnes in 2024, with China and India leading output growth. Their expanding capacity to supply local, regional, and export markets is expected to continue reshaping the industry, challenging established players in Europe and North America.