Regional Processing Hubs Reshape Global Frozen Fries Trade

The global frozen fries industry is entering a new phase of development as production capacity expands beyond traditional exporting regions and moves closer to rapidly growing consumer markets, according to a new analysis by DCA Market Intelligence.

While the European Union remains the world’s largest producer and exporter of frozen fries, the report suggests future growth will increasingly be driven by regional processing hubs serving local demand rather than long-distance international trade.

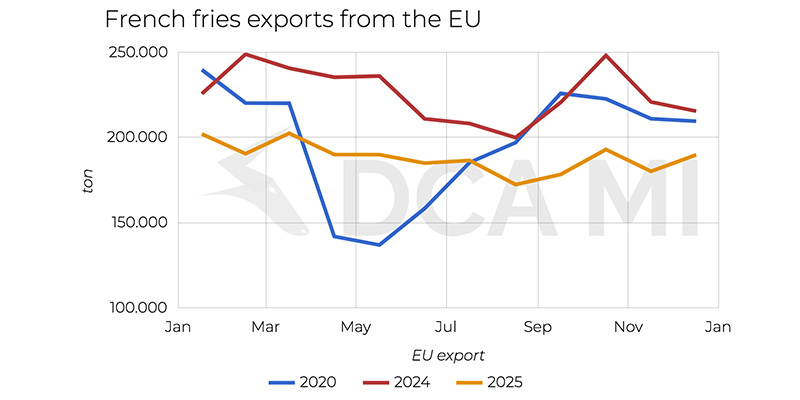

According to DCA Market Intelligence, EU frozen fries exports increased by 24.9% between 2020 and 2025, reaching 6.16 million tonnes. However, much of that growth came from trade within the bloc. Intra-EU exports expanded by 34.9% to 3.54 million tonnes in 2025, while exports to destinations outside the EU peaked at 2.86 million tonnes in 2023 before declining to 2.62 million tonnes in 2025.

The trend points to a broader restructuring of the global frozen potato products market. As consumption accelerates in emerging economies, processors are increasingly locating production closer to end consumers, reducing reliance on imports from Europe and North America.

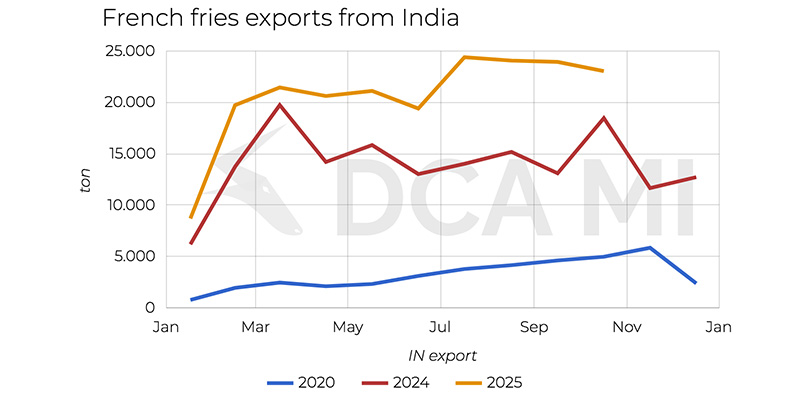

DCA Market Intelligence identifies China, India and Egypt among the fastest-growing frozen fries exporters. Based on UN Comtrade data cited in the report, Chinese frozen fries exports increased by more than 500% between 2020 and 2024, while export value rose by 535% to USD 260.1 million. During the same period, India’s export volume expanded by 421%, while Egypt recorded export value growth of approximately 366% and export volume growth of 194%.

Although these countries remain considerably smaller exporters than the European Union, their growth rates significantly exceed those of traditional suppliers. More importantly, the expansion is taking place in regions where frozen fries consumption is rising most rapidly.

The report highlights rising disposable incomes, urbanization and the continued expansion of quick-service restaurant chains as major drivers of demand growth across Asia, the Middle East, North Africa and parts of South America.

To serve these markets more efficiently, countries are investing heavily in domestic processing capacity. DCA Market Intelligence notes that China and India have expanded processing infrastructure through investments by major international potato processors including McCain Foods, Lamb Weston, Farm Frites, Agristo and Aviko. Egypt has strengthened its position as a supplier to Mediterranean and Gulf markets, while Brazil has increasingly expanded local processing capacity to reduce dependence on imports.

Despite the changing geography of production, the report finds that global frozen fries pricing remains closely interconnected.

EU export prices increased by approximately 69% to EUR 1,279 per tonne in 2023 and are expected to stabilize at around EUR 1,232 per tonne by 2025. Similar trends were observed in North America, where US export prices rose by approximately 45% to USD 1.68 per kilogram in 2024, while Canadian export prices increased by around 35% to USD 1.38 per kilogram.

According to DCA Market Intelligence, export prices in emerging producing countries have also remained within a comparable range. Between 2023 and 2024, export prices in China, India and Egypt generally fluctuated between USD 1.00 and USD 1.40 per kilogram, suggesting that frozen fries are increasingly traded within a common global pricing framework despite the emergence of new suppliers.

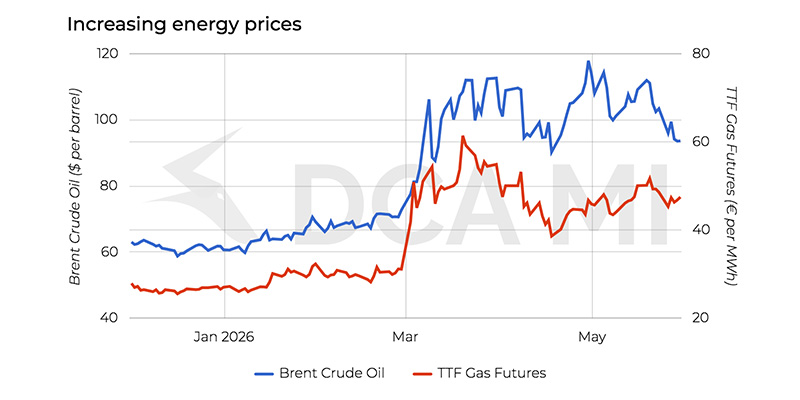

The report argues that this pricing convergence reflects the transmission of cost pressures across major producing regions. Energy costs, in particular, played a central role during recent years. TTF natural gas prices increased from EUR 14.85/MWh in 2020 to EUR 132.41/MWh in 2022 before declining in subsequent years, while processors worldwide faced higher packaging, labor, logistics and production costs.

DCA Market Intelligence notes that energy markets continue to respond to geopolitical developments, with both European gas prices and Brent crude oil prices experiencing renewed upward pressure following recent tensions in the Middle East.

As a result, export prices increased simultaneously across Europe and North America, demonstrating the continued integration of global frozen fries supply chains. Rather than creating isolated regional markets, the emergence of new suppliers has occurred within a globally connected cost and pricing environment.

According to the analysis, the rise of regional processing hubs should therefore be viewed as a reorganization of supply chains rather than a fragmentation of the industry. By locating production closer to consumers, processors can reduce transportation distances, lower cold-chain costs, improve delivery times and limit exposure to disruptions affecting long-distance trade routes.

At the same time, DCA Market Intelligence cautions that the geographical diversification of production does not necessarily translate into a diversification of market power. Much of the new processing capacity is being developed by the same multinational companies that have historically dominated the frozen fries sector through investments in processing facilities, contract farming systems, cold storage infrastructure and technical support networks.

As a result, the industry is evolving toward a model characterized by a more geographically distributed production base while remaining relatively concentrated in terms of ownership and influence.

According to DCA Market Intelligence, Europe remains the dominant exporter, but its position is increasingly being challenged by regional suppliers capable of serving nearby markets more efficiently. Future growth is likely to depend less on long-distance exports and more on regional processing hubs designed to supply rapidly expanding consumer markets.

For the frozen fries industry, the regionalization of production appears less a sign of fragmentation than the next stage in the evolution of a globally connected market.