European Potato Market Faces Structural Oversupply As Prices Turn Negative

The European potato market is experiencing acute downward pressure, with prices in some segments falling below zero as growers struggle to manage a significant surplus, according to DCA Market Intelligence.

An oversupply built over the past two growing seasons has collided with weakening demand, leaving producers across Northwestern Europe with limited market outlets. In extreme cases, growers are now paying to dispose of potatoes, as traditional channels—including free distribution—fail to absorb excess volumes.

Expansion Meets Demand Contraction

The imbalance follows a period of aggressive acreage expansion in the Netherlands, Belgium, Germany, and France. Encouraged by strong processing demand and favorable contract prices, farmers increased production significantly. This was compounded by favorable growing conditions in 2025, which delivered high yields and a substantial harvest.

However, export conditions have deteriorated. Increased competition from Asian suppliers, U.S. import tariffs, and a weaker dollar have eroded the competitiveness of European potatoes in global markets. The result is a structural surplus that the domestic market is unable to absorb.

Prices Reflect Market Breakdown

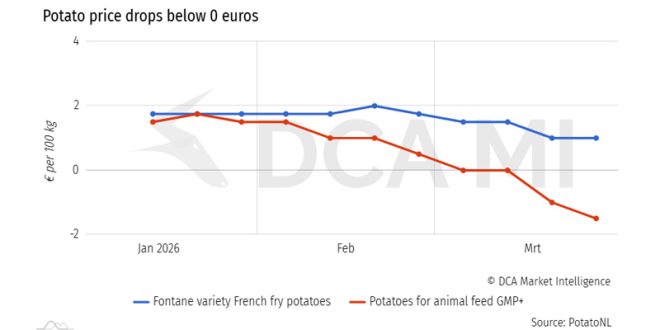

Market signals underline the severity of the imbalance. Recent price data from PotatoNL show values for animal feed potatoes ranging from €-1.00 to €-2.00 per 100 kilograms. Even processing-grade potatoes for French fries are only marginally higher.

As a result, increasing volumes are being diverted to lower-value outlets such as animal feed and anaerobic digestion. Disposal costs are frequently being borne by growers, a situation exacerbated by rising transport expenses.

Storage Constraints Accelerate Market Pressure

Although potatoes can be stored for extended periods, the economics of storage are rapidly deteriorating. With no clear prospect of price recovery, growers are choosing to release stocks earlier to avoid incurring additional cooling and storage costs.

“Not everyone can store their potatoes for that long. Moreover, there is currently no outlook for market improvement. As a result, growers are deciding to stop incurring cooling costs,” said Niels van der Boom, potato market specialist at DCA Market Intelligence.

This behavior is accelerating the flow of additional volumes onto an already saturated market, while simultaneously creating urgency to free up storage capacity ahead of the next harvest.

Surpluses Mount Across EU-4

The scale of the surplus across the EU-4—Netherlands, Belgium, France, and Germany—is substantial. In the Netherlands alone, the 2025 harvest reached approximately 4.2 million tonnes of ware potatoes, around 900,000 tonnes higher than the previous year. Despite some diversion to feed, digestion, and starch processing, an estimated 500,000 to 600,000 tonnes remain unsold.

Elsewhere, Belgium is reported to have around 800,000 tonnes in storage without buyers, while France faces a surplus of approximately 1 million tonnes. Germany is expected to report a similar volume. In total, DCA Market Intelligence estimates that the EU-4 surplus stands at roughly 3.3 million tonnes.

Industry Responses Emerging

Efforts to manage the excess supply are beginning to take shape, though responses remain fragmented. In Belgium, promotional campaigns are being deployed to redirect potatoes into food, feed, and biogas applications. In France, industry bodies including GIPT and Arvalis are developing protocols for controlled destruction to mitigate potential health risks.

In contrast, the Netherlands has yet to implement concrete measures, despite ongoing discussions within the sector. Given the scale of the surplus, stakeholders face mounting pressure to establish coordinated solutions that can accommodate the upcoming harvest.

Structural Adjustment Required

The current situation highlights a broader need for recalibration across the European potato value chain. Production planning, contracting strategies, and market development efforts will need to be reassessed to align with shifting global demand dynamics and increased market volatility.

Without such adjustments, the sector risks prolonged periods of oversupply and continued price instability.